Measuring obesity

Obesity is a public-health concern throughout the developed world, since it is linked to a variety of chronic conditions such as diabetes. Obesity is also of interest to insurers, since it is linked to excess mortality from a wide range of causes, including heart disease. The most commonly used measure of obesity is the body-mass index (BMI), which is calculated from a person's height and weight. The British Heart Foundation has an online BMI calculator which is free to use.

Now, the United Kingdom doesn't often take a leading role in the EU, but sadly obesity is one area where it rather stands out, as shown in Table 1.

Table 1. Prevalence of obesity among adults in selected large EU countries (Source: Health Interview Surveys, European Commission: Eurostat)

| Percentage obese |

EU Country |

|---|---|

| 22.7 | England |

| 20.3 | Germany |

| 13.3 | Spain |

| 11.4 | Poland |

| 9.3 | France |

| 8.1 | Italy |

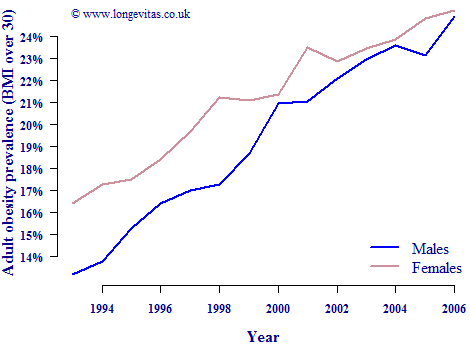

The prevalence of obesity in England has risen dramatically in recent years, as shown in Figure 1. Men have lower rates than women, although the gap has narrowed meaning that male obesity prevalence has risen faster.

Figure 1. Adult obesity prevalence in England (Source: Health Survey for England 2006)

Some commentators argue that rising obesity levels will undo some of the advances in life expectancy seen over the past decades. At a population level this may well be true, as Table 1 and Figure 1 above suggest. However, this does not necessarily read across to life-assurance business or pension funds. We saw in an earlier post how a large proportion of liabilities are concentrated in a relatively small number of lives, and Table 2 shows that there are differences in obesity prevalence by income group.

Table 2. Obesity prevalence by income quintile (Source: Health Survey for England 2006.)

| Income quintile |

Males | Females |

|---|---|---|

| Highest | 21 | 19 |

| 2nd | 23 | 23 |

| 3rd | 24 | 24 |

| 4th | 27 | 29 |

| Lowest | 25 | 32 |

Table 2 reminds us that results from population data may not be appropriate for insured liabilities, which actuaries call basis risk. Indeed, it is not hard to imagine widening socio-economic differentials slowing or halting mortality improvements at the population level at the same time as insured lives continue to see robust improvements. This is one reason why we put so much emphasis on using all available information to assess socio-economic status.

Add new comment