A basis point

In an earlier post I mentioned the advent of survivor forwards, or S-forwards, a derivative contract which could be used for hedging pension liabilities. Survivor forwards appeared again in another post illustrating the financial impact of model risk.

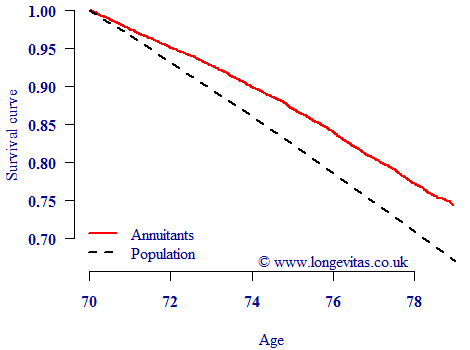

A survivor forward defined on an index of, say, population mortality will give a large data set with considerable history on which to base a projection model. However, a natural question is to ask how suitable such a contract would be for hedging pension or annuitant liabilities? Figure 1 shows the Kaplan-Meier survival curve from age 70 for male annuitants born in 1928, together with the corresponding survival curve for males in England & Wales.

Figure 1. Survival curves for male annuitants (red line) and males in England & Wales (black line). Source: Own calculations using ONS data for males in England and Wales, 1998–2006, and life-office annuitants over the same date range.

Figure 1 shows that life-office annuitants have a markedly higher survival rate than the population at large. This is unsurprising: people who have private pensions form a wealthier (and healthier) select sub-group of the wider population. However, one consequence of this is that a survivor forward defined on population mortality will in general be an imperfect hedge for most annuity portfolios or pension schemes. This is known as basis risk, and is well-known in other industries. For example, airlines cannot hedge their jet-fuel costs directly, and so use imperfect hedges based on crude-oil or heating-oil futures.

As it happens, there are solutions to the divergence shown in Figure 1. One solution is for the pension scheme to buy varying proportions of the underlying S-forwards to replicate the anticipated higher survival curve of holders of private pensions. Another solution was discussed by Iain Currie in his post on modifying projections for basis risk.

Add new comment