A second pension-scheme revolution

In his book Unseen Revolution, Peter Drucker drew attention to the structural changes in economic ownership which were silently ushered in with the growth of corporate pension schemes. Decades later these changes had turned the pension scheme into the dominant item on some companies' balance sheets. Other companies experienced even more dramatic consequences.

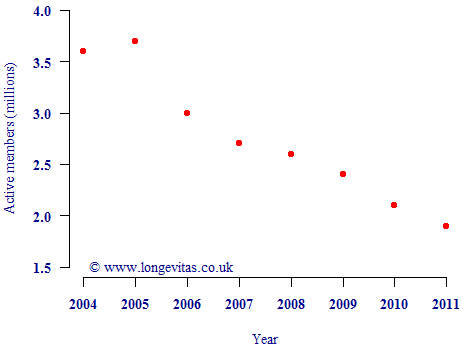

However, there is currently a second revolution underway amongst UK pension schemes, at least in the private sector. This revolution will have a large impact on the corporate landscape. To illustrate why, we begin with the number of active members of private-sector, defined-benefit pension schemes in the UK, i.e. working people accruing benefits, as shown in Figure 1.

Figure 1. Active members of private-sector, defined-benefit pension schemes in the UK. Source: Occupational Pension Schemes Survey (OPSS) annual report 2011, Table 3.3.

Figure 1 shows that the number of active members of UK defined-benefit pension schemes has halved in six years. This shows the speed with which UK companies are closing their schemes to new members (or, as is increasingly the case, to future accrual for existing members as well). If the rate of decline shown in the last four years of Figure 1 continues, by 2021 there will be a negligible number of active members of private-sector, defined-benefit schemes.

Some commentators will be interested in the societal aspects of this shift, such as how younger workers will not see the sort of pension benefits enjoyed by their (grand-)parents. Others will be interested in the political aspects, such as how defined-benefit pensions will shortly be the preserve of public-sector workers only. However, there will be consequences for the closed schemes themselves, one of which will be a rapid ageing of the liability profile. Without younger new entrants the average age of the scheme membership will increase steadily every year. This will change the focus of risk management, as some aspects of longevity risk change with increasing age. And without accrual of new benefits the cashflow position of schemes will change — the point at which schemes have to sell assets to pay pensions will be brought forward, which will change investment policy.

Finance directors could be forgiven for thinking that the company pension scheme is a thankless game of "whack-a-mole" — you close the scheme to new entrants or future accrual to stop the problem growing, only to find out that new challenges pop up elsewhere due to changes in the scheme's liability profile. Fortunately for finance directors, there are more options for risk management than ever before, including relatively new tools such as longevity swaps and even forward contracts. For those seeking a more comprehensive solution, the bulk-annuity market allows a scheme to pass all its risks to an insurer. As this second pension-scheme revolution quietly nears completion, expect continued growth in risk-management activity over the next decades.

References:

Drucker, P. F. (1976) The Unseen Revolution, Harper & Row.

Add new comment